American + Alaska JV Isn't a Smaller Merger. It's the First Step of a Bigger One.

American and Alaska are reportedly negotiating Alaska's entry into AA's joint ventures with British Airways, Iberia, Finnair, Aer Lingus, and Japan Airlines. Most coverage reads this as the consolation prize for a merger that won't happen. The cleaner read: a JV is the move you make before a merger, not instead of one.

Bloomberg broke the news on April 22 that American is in early talks with Alaska Air Group on a revenue-sharing partnership. Reuters, Skift, and TPG matched within hours. The reported scope is specific. Alaska would join American's Atlantic joint business — currently AA, British Airways, Iberia, Finnair, and Aer Lingus. Alaska would also join the AA / Japan Airlines transpacific JV. Coordinate schedules, fares, capacity. Pool revenue inside the JV. Requires DOT antitrust immunity, which has not been filed.

Much of the coverage reads the deal as the smaller version of a merger — what AA settled for after a takeover wasn't on the table. That isn't quite the right read.

A JV answers the partnership-economics questions a merger has to answer first. Who flies the metal on a given route. Who captures the revenue when an Alaska passenger connects to a BA transatlantic. How schedules get coordinated so the partners don't compete for the same connecting passenger. What an Alaska elite gets on an AA-marketed itinerary, and vice versa. These are the questions integration teams chew through for two years after a merger announcement. A JV makes you answer them on the front end.

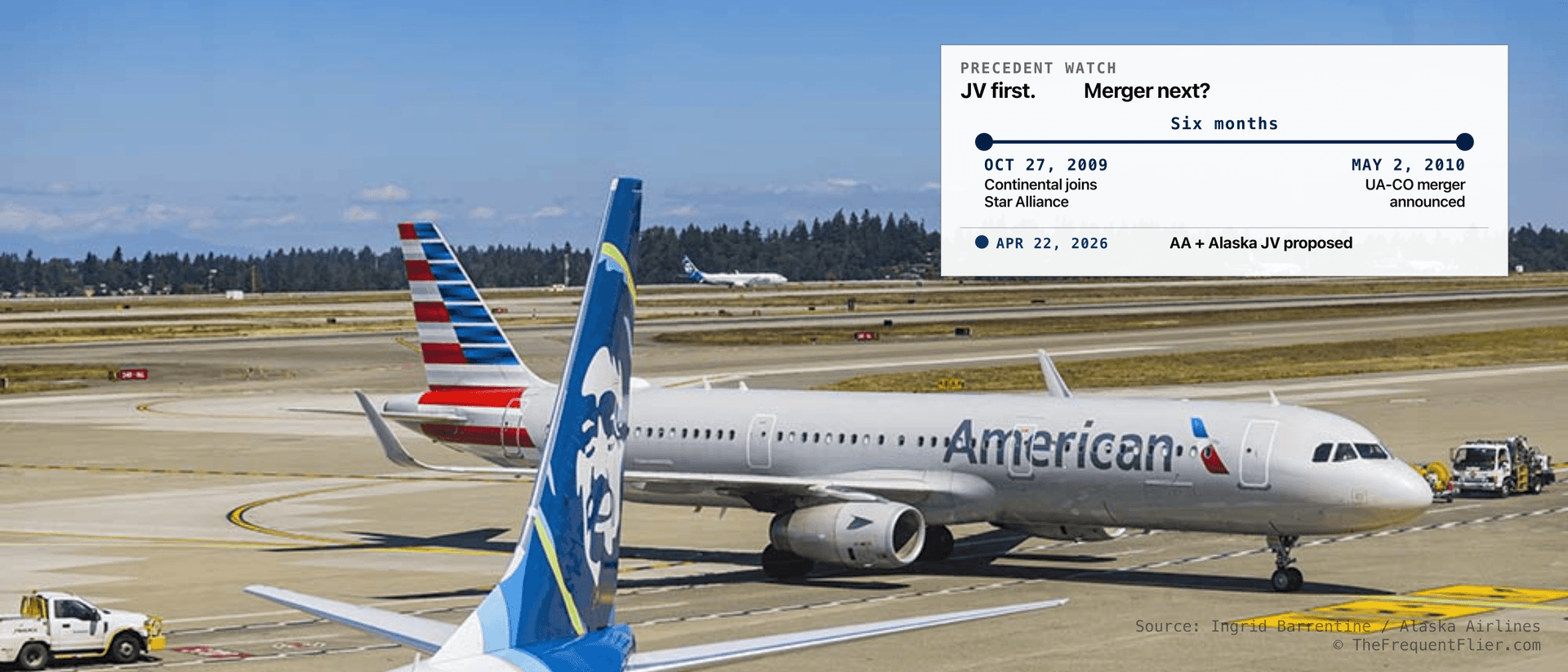

The precedent

There's a recent precedent for what that sequence looks like.

In June 2009, Continental announced it was leaving SkyTeam and joining Star Alliance. The DOT cleared the transatlantic A++ joint venture (UA, Continental, Lufthansa, Air Canada) the next month. Continental switched alliances on October 27, 2009. Six months later, on May 2, 2010, United and Continental announced an $8.5 billion merger of equals. The integration was a continuation of the JV work. Same teams, same routes, same coordinated revenue. The merger was the legal wrapper around an operational integration that had already started.

Continental → United

OCT 27, 2009 to MAY 2, 2010Six months

- JUN 2009CO announces Star Alliance move

- JUL 2009DOT clears A++ JV (UA, CO, LH, AC)

- MAY 2, 2010UA-CO merger announced

- OCT 1, 2010Merger legally complete

Alaska → American

MAY 2026We are here

- APR 22, 2026Bloomberg reports JV talks

- ForwardDOT antitrust immunity filed

- ForwardMerger conversation re-opens

A JV is the move you make before a merger, not instead of one.

Not every JV ends in a merger. AA spent fourteen years getting antitrust immunity on the BA/Iberia transatlantic JV, and the combination has stayed three independent carriers. The JV is the precondition that makes a merger commercially feasible if the structural conditions are there. It doesn't manufacture them.

The structural conditions

The structural conditions for AA + Alaska are there.

Alaska runs no antitrust-immunized international JVs of its own today. Its long-haul international program is in its earliest stages — Tokyo launched in May 2025, Seoul is on the schedule. The international bench Alaska wants is the bench AA already operates. AA is the inverse case: a strong international JV footprint attached to a thin West Coast network. UA dominates SFO. Alaska and DL split SEA between them, with AA never a meaningful presence. LAX is AA's only sizable West Coast hub — and DL has grown against it there too. The geographic complementarity isn't a merger pitch. It's the operating reality both carriers manage either way.

SEA — passenger share, Q1 2025

- Alaska

- 43% (Apr peak 52%)

- American

- <5%

- Delta

- 20% (Apr peak 24%)

- United

- small

- Other

- balance

SFO — departure share, 2024

- Alaska

- 10%

- American

- 6%

- Delta

- 7%

- United

- 47%

- Other

- balance

LAX — passenger share, H1 2024

- Alaska

- ~6%

- American

- 16%

- Delta

- 19%

- United

- 15%

- Other

- WN ~13%, balance

The JV captures most of the commercial benefit without DOJ merger review, without a single operating certificate, and without the pilot seniority-list integration that's still hung up the Alaska / Hawaiian deal a year after the customer-facing side of that merger finished. AA's last integration ran two years to a single operating certificate, and longer to feel integrated. A JV produces real numbers in eighteen months.

What Isom said on the call

Read the Q1 earnings call closely. AA CEO Robert Isom didn't confirm scope, but he said American was at the "forefront" of partnership and "asset acquisition" opportunities. He called Alaska "fiercely independent." Both phrases are doing work. Asset acquisition keeps the merger door open. Fiercely independent signals that AA understands Alaska's leadership isn't going to be absorbed.

The clean version of the merger thesis was never that AA buys Alaska. It was that the Alaska / AA combination eventually makes sense, and that Alaska's operating discipline is what AA needs. The JV is how you build the case. Run the partnership for three to five years. Show regulators the consumer benefit. Show the unions a path that doesn't blow up either seniority list. Show the boards a combination that already works commercially. Then file.

The "consolation prize" framing isn't wrong about the present state. It misreads what the present state means for the next state. The deal AA is reportedly negotiating is simultaneously what the carrier had to settle for in 2026 and the dress rehearsal for the integration it might attempt at the back end of the decade. Both are true.

The more interesting question is whether Isom is the executive who runs that play. Four years of stock underperformance, two unions on no-confidence, peers 31–45× more profitable on adjusted operating margin. The board has had every reason to have already moved on. They haven't. Once a partnership of this scale starts producing the numbers a successor would inherit, the choice gets harder to keep deferring — and the successor inherits the choreography, not the question of whether to dance.

Agree or disagree?

Tell me what I missed, what you'd add, or where the argument breaks.