Gulf Carriers Are Taking Back the Europe Traffic Asian Airlines Borrowed

Emirates, Qatar Airways, and Etihad carried a third of Asia–Europe passengers before the Iran war closed their hubs. Their schedules are back to roughly 90% — and the record loads Asian carriers posted all spring are deflating month by month.

Before February 28, Emirates, Qatar Airways, and Etihad carried nearly one in three passengers flying from Asia to Europe, and more than half of those flying from Australia and New Zealand, according to Cirium schedule data. Then US and Israeli strikes on Iran set off retaliation across the Gulf. Drone and missile attacks closed Dubai and Doha. Qatar Airways canceled the vast majority of its schedule in the first month. All that connecting traffic didn't disappear — it went looking for another routing.

It found two: nonstop flights on Asian carriers, and Istanbul. Singapore Airlines' load factor to Europe — the percentage of seats filled — jumped 13.8 points year-over-year in March. ANA's Europe flights ran 93% full. Cathay Pacific's network-wide load factor hit 92%. Turkish Airlines carried 7.2 million passengers in March, up 16% from a year earlier. Planes were full, discount fares vanished, and almost none of it required adding a single flight.

The Gulf comeback has been faster than the spring's booking hesitancy suggested it would be. By mid-June, Gulf carriers' flights were back to roughly 90% of normal levels, per Flightradar24 data. Qatar Airways passed 150 destinations on June 16 and put A380s back on London Heathrow and Bangkok the same day. Emirates says it has restored about 96% of its destination map, though weekly frequencies are still around three-quarters of pre-war levels. Etihad is discounting aggressively to pull traffic back. And in June, Australia lifted the "do not travel" advisory that had been voiding travelers' insurance at Gulf hubs — Flight Centre says its bookings on the three carriers rose 36% the following week.

The windfall had a half-life

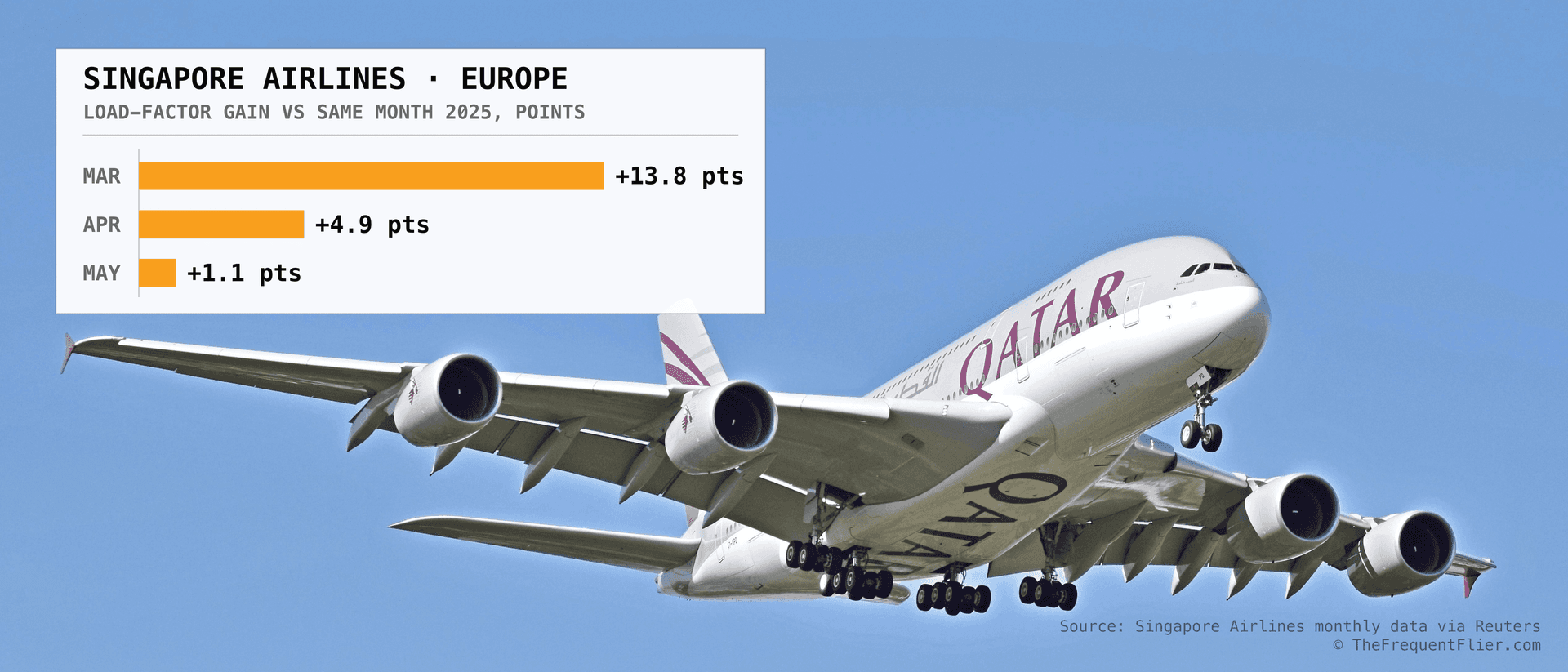

The rebalancing shows up cleanly in the monthly numbers. Singapore Airlines' Europe load-factor gain went from +13.8 points in March to +4.9 in April to +1.1 in May. ANA's Europe load factor slipped from 93.1% in March to 86.9% in April — still 8.7 points better than a year earlier, but pointed the same way. Cathay's year-over-year gain narrowed from 9.5 points to 2 by May. The International Air Transport Association's data tells the mirror-image story: Middle Eastern carriers went from a 60% passenger decline in March to a 28% decline in May. Nonstop Asia–Europe traffic, up nearly 30% in March, was up 15% by May. "In May the load factors for both Europe and Australia normalized," independent analyst Brendan Sobie told Reuters. Gradual, not overnight. One direction.

Year-over-year load-factor gain, by month

Percentage points vs. same month 2025

The load factors also hide a lag worth understanding. Long-haul tickets book on roughly a six-month window, which means much of what Asian carriers sold at windfall fares in March and April hasn't been flown yet. BofA's Nathan Gee made exactly this point: the peak of the load-factor gains has passed, but "the strongest contribution to flown revenues will be seen in the upcoming quarters." Singapore Airlines, Cathay, Korean Air, and ANA will book much of the windfall's revenue after the traffic that produced it has started going home.

What doesn't snap back

The sky itself is the other asymmetry. Kuwait's airspace remains closed to overflights until at least August 4. Western Iran is still heavily restricted. Europe–Asia flights still detour south over Egypt and Saudi Arabia or north over the Caucasus and Afghanistan, and GPS jamming is now a routine operational hazard across the region. The Gulf hubs are selling a near-full schedule flown across a still-bent map. The frequencies are back before the efficiency is.

Meanwhile, capacity decisions made during the windfall are landing now. Singapore Airlines goes from daily to ten weekly flights to Amsterdam between August 1 and October 22, on top of recent additions in Manchester, Milan, and Munich, a double-daily London Gatwick operation, and a new Madrid service. That is either capacity arriving just as the peak passes, or a bet that enough of the borrowed traffic can be kept. The winter timetable will show which read was right.

Emirates

- Where things stand (late June)

- About 96% of destinations restored; weekly frequencies around three-quarters of pre-war levels

- What to watch

- Baghdad, Basra, and Tehran remain suspended

Qatar Airways

- Where things stand (late June)

- 150+ destinations as of June 16; A380s back at Heathrow and Bangkok

- What to watch

- Rebuild pace toward the full pre-war network

Etihad

- Where things stand (late June)

- Discounting aggressively to rebuild connecting traffic

- What to watch

- How long the fare sale lasts

Singapore Airlines

- Where things stand (late June)

- Europe load-factor gain down to +1.1 points in May

- What to watch

- Amsterdam goes 10x weekly Aug 1–Oct 22, pending approvals

Cathay Pacific

- Where things stand (late June)

- Network-wide load-factor gain narrowed to +2 points in May

- What to watch

- Whether any windfall share holds as Gulf fares fall

Turkish Airlines

- Where things stand (late June)

- 7.2 million passengers in March, up 16% year-over-year

- What to watch

- Growth cooling as the Gulf reopens

For travelers, the direction is friendly either way. The fare premium for avoiding the Gulf is deflating, seats on the Asian nonstops are reappearing, and the one-stops through Doha and Dubai are pricing to win you back. Borrowed traffic returns on the lender's terms.

Agree or disagree?

Tell me what I missed, what you'd add, or where the argument breaks.