IATA Halved Its 2026 Airline Profit Forecast. The Same Fuel Shock Hits Six Regions Six Different Ways.

The industry's fuel bill jumps from $252 billion to $350 billion this year, and profits shrink to $23 billion. The regional table underneath is the story: the Middle East swings from the world's best per-passenger profit to its worst, Europe's hedges buy a year, and largely unhedged North America keeps the top of the ladder anyway.

IATA used its annual meeting in Rio on June 7 to cut the industry's 2026 outlook roughly in half. Airlines are now expected to earn $23 billion this year. The December projection was $41 billion. Last year's actual was $45 billion. The cause is not a mystery: jet fuel is expected to average $152 a barrel in 2026, up almost 70% from last year, and the industry's fuel bill rises from $252 billion to $350 billion. Willie Walsh put the result in concrete terms — profit per passenger falls to $4.50, which as he noted won't even buy a hot dog at most of the World Cup venues.

The global number is real, but it's an average, and the average hides the event. The same fuel shock is producing six different outcomes in six regions. 2026 isn't shrinking the industry evenly. It's sorting it.

The per-passenger ladder

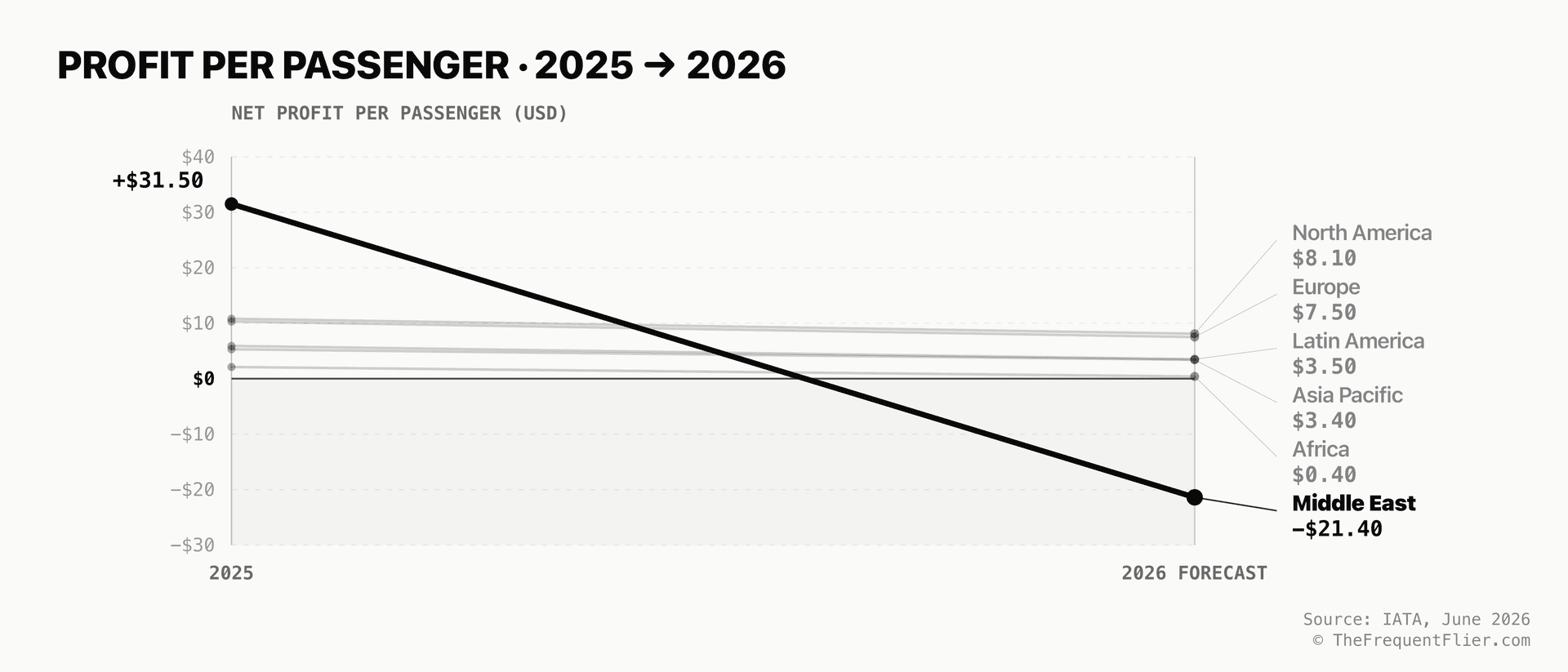

Profit per passenger is the cleanest view of the sort. In 2025, Middle East carriers earned $31.50 per passenger — the best in the world, by a wide margin. In 2026, IATA expects them to lose $21.40 per passenger — the worst. That's a swing of roughly $53 per passenger in a single year, driven by airspace closures, cancelled flights, and the loss of the transfer traffic the Gulf hub model is built on.

Profit per passenger, 2025 → 2026 forecast

The rest of the ladder: North America keeps $8.10 per passenger. Europe keeps $7.50. Asia Pacific and Latin America hold around $3.50. Africa keeps 40 cents.

Africa is the ladder's strangest rung. African carriers are growing traffic faster than anyone — demand is up 10% as Europe–Asia routings bend south around the war zone. Almost none of it converts to profit. Fuel supply on the continent is expensive and unreliable, aircraft fly fewer hours per day, and balance sheets are too thin to absorb the difference. More passengers, a 0.2% margin. Traffic is not the same thing as a business.

North America

- 2026 net profit

- $9.4B

- 2026 net margin

- 2.5%

- Profit / passenger 2026

- $8.10

- Profit / passenger 2025

- $10.80

- Demand growth

- +0.8%

Europe

- 2026 net profit

- $9.6B

- 2026 net margin

- 3.1%

- Profit / passenger 2026

- $7.50

- Profit / passenger 2025

- $10.30

- Demand growth

- +2.8%

Latin America

- 2026 net profit

- $1.2B

- 2026 net margin

- 2.1%

- Profit / passenger 2026

- $3.50

- Profit / passenger 2025

- $5.90

- Demand growth

- +5.0%

Asia Pacific

- 2026 net profit

- $6.6B

- 2026 net margin

- 2.1%

- Profit / passenger 2026

- $3.40

- Profit / passenger 2025

- $5.30

- Demand growth

- +5.1%

Africa

- 2026 net profit

- $0.1B

- 2026 net margin

- 0.2%

- Profit / passenger 2026

- $0.40

- Profit / passenger 2025

- $2.10

- Demand growth

- +10.0%

Middle East

- 2026 net profit

- −$4.3B

- 2026 net margin

- −6.1%

- Profit / passenger 2026

- −$21.40

- Profit / passenger 2025

- $31.50

- Demand growth

- −11.4%

What's doing the sorting

Three variables separate the regions, and none of them is demand.

The hedge book. Globally, airlines have hedged about a third of this year's fuel. Europe came into the crisis at 70% — which is most of why European carriers keep $7.50 a passenger despite importing most of their jet fuel from the Gulf. But there's a catch inside the hedges: many airlines hedge crude oil, not jet fuel, because the crude market is deeper. The crack spread — the premium refiners charge to turn crude into jet fuel — is expected to average $57 a barrel this year, a record. A crude hedge doesn't cover that. And every hedge rolls off eventually.

Share of 2026 fuel needs hedged

% of expected 2026 fuel consumption hedged

Geography. The Middle East sits at the center of the shock. Asia Pacific sits next to it. The region imports Gulf crude, so refinery pressure and spot shortages push its jet fuel prices above other regions'. Airspace detours add fuel burn on top, and weak local currencies make dollar-priced fuel dearer still.

Pricing power. North American carriers hedge almost nothing — IATA notes the fuel shock reaches their cost base about as directly as it can. They still keep more profit per passenger than any region in the world. The mechanism is the adjustment IATA politely calls "predominantly price-driven": capacity grows 0.3% — effectively flat — and fares carry the shock straight to the customer. Nobody had to coordinate that. IATA also names who pays for it inside the region: low-cost carriers without a premium cabin have no upsell lever, and the gap between them and the network carriers widens.

The sort doesn't decide who thrives. It decides who suffers comfortably — and who doesn't get to.

The 2008 echo

I remember the 2008 spike. IATA's release reaches for the same comparison — unit revenues haven't grown this fast outside the COVID rebound since 2008 and 2010. The difference is what the industry has become since. Planes are 84% full, a record. Ancillary revenue passes cargo this year for the first time since 2019. Premium cabins give the strongest carriers a fare ladder to climb that didn't exist in 2008 — IATA's own North America section credits exactly that segmentation. Back then, a fuel spike was a catastrophe to be survived. In 2026, for the carriers built for it, it's a bill that gets forwarded.

Forwarded is not the same as escaped. Even after repricing, the industry earns 4.3% on invested capital this year, against a cost of capital around 8.5%. The sort doesn't decide who thrives. It decides who suffers comfortably — and who doesn't get to.

Agree or disagree?

Tell me what I missed, what you'd add, or where the argument breaks.